THIS WEBSITE INCLUDES GENERAL INFORMATION & THE OPINIONS OF CHRISTOPHER S. MULVANEY. IT IS INTENDED TO STIMULATE A BASIS FOR QUESTIONS RELATED TO YOUR PARTICULAR FACTUAL CIRCUMSTANCES — BEFORE YOU ACT. THIS WEBSITE DOES NOT CONSTITUTE LEGAL ADVICE. IF YOU WANT LEGAL ADVICE, PLEASE MAKE A ZOOM APPOINTMENT TO SPEAK WITH ME.

CONTACT CHRISTOPHER S. MULVANEY FORM

DISCLAIMER:

The use of email or this form for communication with MULVANEY LAW OFFICE, PLLC does not establish an Attorney-Client Relationship. If you don’t think I have responded, please check your spam folder. Time-sensitive information should not be sent through this Form or through email. Sensitive information can be uploaded to an encrypted Dropbox folder in your client file. Google Review LinkYelp Review Link

Gonzaga University School of Law – Spokane, Washington – Class of 2002 – Cum Laude The Latin phrase “Deo patriae, scientiis, artibus” translates to “For God and country through sciences and arts”. The initials A.M.D.G. on the seal of Gonzaga Law School stand for Ad Majorem Dei Gloriam, which is Latin for “For the Greater Glory of God” the Motto of the Society of Jesus (Jesuits): a Catholic religious order founded by St. Ignatius of Loyola.

_________________________

“Each time a man stands up for an ideal, or acts to improve the lot of others, or strikes out against injustice, he sends forth a tiny ripple of hope, and crossing each other from a million different centers of energy and daring those ripples build a current which can sweep down the mightiest walls of oppression and resistance.” – Robert F. Kennedy (1925-1968, American Attorney General, Senator)

COLLATERAL/SECURITY

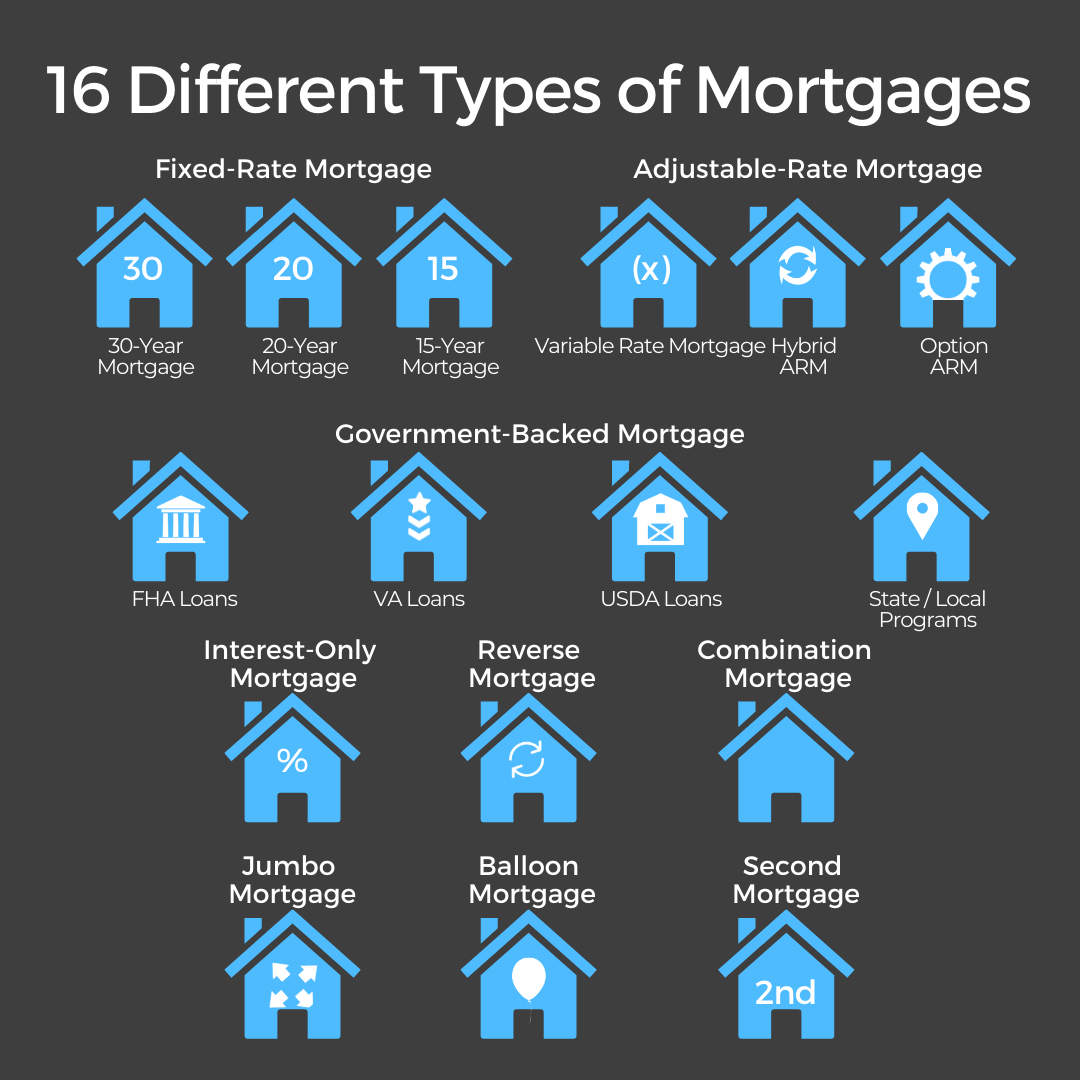

A Deed of Trust pledges real estate as security for a Promissory Note as does a Mortgage. There are different types of mortgages.

One that is not on the above chart, has the potential to make housing more affordable to low income people without many prospects for increasing their income. That is the Negatively Amortized Mortgage. My sister has one that she obtained through the Spokane Neighborhood Action Programs. She pays something like $400 per month. Nothing goes to principle and the payment isn’t quite enough to cover the interest. So, the mortgage balance is growing as the house is appreciating in value. These are occurring at approximately the same rate with appreciation slightly outpacing interest growth. She put nothing down. What that means is that when she dies, the bank takes the house back and resells it. The interest that the bank received during my sister’s life and after she dies is revenue to the bank. I am not sure how much the taxpayers pay or precisely how it is paid to get lenders to offer a place to live for people like my sister who have no “skin in the game.” Whatever it is, it has made a world of difference. My sister has lived in the house for 30 years and will die there. She can’t find that kind of affordable housing anywhere else in this Country. She owns title to the house, even though she doesn’t have equity which makes her eligible for several different types of low income homeowner aid (to fix her roof and pipes for example). She also gets energy assistance and food stamps and social security disability with the broad medical coverage she needs. If we can let go of the idea of equity building and just let people like my sister care for the house, which she does, and live there for decades. The bank gets to capture all of the appreciated value of the home. Normally, if a home is sold, the bank gets the balance on the Promissory Note and the Homeowner (or heirs) get any amount above that. The bank has an income stream, no default, good home maintenance, and gets all of the appreciated value on top of the accrued interest from the slightly short monthly payments. Government assistance of this type could help a lot of people. My sister’s daughter’s father is Mexican. Her name is a Mexican name, so she got the house as a government benefit for low-income Hispanic families.

You signed a security instrument when you bought your house. You have to have made a promise to pay before you can pledge your home equity as collateral for that promise.

A Deed of Trust does need to be Notarized (unlike a Promissory Note) because it must be Recorded and provides much more protection because it is a security interest – a lien.

A Deed of Trust pledges real estate as collateral for the promise to pay and is required to be paid by Escrow if the property is refinanced or sold. Security Interests such as those created by Deeds of Trust survive the Bankruptcy Discharge and must be paid by the equity in the property (even though the Debtor cannot be garnished or have their bank account attached for the debt following the Bankruptcy Discharge).

The Deeds of Trust that I prepare do not contain the ability to accelerate the loan and foreclose because I typically represent both Parties, so I have to be fair to both. Securing the debt, but having to wait for a refinance or sale is fair. Allowing foreclosure is not fair.

The Deed of Trust must be Recorded to be effective.

A deed of trust, also known as a trust deed, is a legal document used in real estate transactions, particularly for securing a loan on a property. It’s essentially a type of loan agreement that works differently than a traditional mortgage, particularly in how foreclosure is handled.

Although Mortgage and Deed of Trust are often used interchangeably because they serve the same purpose, there are some technical differences. Washington uses Deeds of Trust primarily which means that most Foreclosures in Washington are Non-Judicial.

While both mortgages and deeds of trust are used in real estate to secure a loan against a property, they differ primarily in the parties involved and the foreclosure process.

Feature

Mortgage

Deed of Trust (Trust Deed)

Parties Involved

Two parties: * Borrower (Mortgagor): The person taking out the loan. * Lender (Mortgagee): The financial institution or entity providing the loan.

Three parties: * Borrower (Trustor): The person taking out the loan. * Lender (Beneficiary): The financial institution or entity providing the loan. * Trustee: A neutral third party (often a title or escrow company) who holds the legal title to the property in trust until the loan is paid off.

Foreclosure Process

Typically involves judicial foreclosure. * The lender must file a lawsuit in court to obtain a judgment and order a foreclosure sale. * This process can be lengthy and expensive.

Typically involves nonjudicial foreclosure. * The trustee has the power of sale and can sell the property without going through the court system if the borrower defaults. * This process is generally faster and less costly than judicial foreclosure.

Who Holds Legal Title During Repayment

The borrower generally holds the legal title, and the lender has a lien on the property.

The trustee holds the legal title until the loan is fully repaid.

Mortgages involve a two-party agreement and typically require judicial foreclosure.

Deeds of trust involve a three-party agreement (including a trustee) and allow for nonjudicial foreclosure in most cases, which can be a quicker process for the lender.

Three-Party Agreement: Unlike a mortgage that involves two parties (borrower and lender), a deed of trust involves three parties:

Trustor (Borrower): The person who is borrowing the money to buy the property.

Beneficiary (Lender): The person or entity lending the money, such as a bank.

Trustee: A neutral third party, typically a title company, escrow company, or bank, who holds legal title to the property until the loan is paid in full.

Security for the Loan: The deed of trust secures the promissory note, which is the borrower’s promise to repay the loan.

Trustee Holds Title: The trustee holds the legal title to the property while the borrower has the equitable title (the right to use and benefit from the property and gain equity as they repay the loan).

Nonjudicial Foreclosure: A key difference between a deed of trust and a mortgage is the foreclosure process. Deeds of trust usually include a power-of-sale clause that allows the trustee to initiate a nonjudicial foreclosure process, meaning they can sell the property without going through the court system, says the Legal Information Institute.

Foreclosure Process: If the borrower defaults on the loan, the trustee, as authorized by the deed of trust, can sell the property through a public auction to recover the outstanding loan amount.

Deed of Reconveyance: Once the loan is fully repaid, the trustee issues a deed of reconveyance, transferring the legal title back to the borrower and releasing the lien on the property.

In essence, a deed of trust is a form of secured real estate transaction where a third-party trustee holds the property’s legal title as collateral for the loan, allowing for a potentially faster and less expensive foreclosure process if the borrower defaults.

Deeds. You can record real estate deeds by mail for $316.50 each (plus postage both ways) which takes about 4 months; or You can use this LawPay Link to charge $400 per deed and I can electronically record only with the King County Recorder, which takes about 1 day. Real Estate Deeds are not effective unless recorded (made a public record) during your life. The emailed PDF of the Deed with the instrument number, date and time of recording is the only proof of electronic recording you will receive. Here are the links to the Snohomish County Recorder and Pierce County Recorder where you should be able to record in person or by drop off after hours.

USE TO PRESERVE SEPARATE PROPERTY EQUITY IN JOINTLY OWNED HOME

For example, if one spouse inherits $500,000 and pays down the mortgage on a home they both live in (even if the home is titled in the inheriting spouse’s name), then it is vitally important to ask the non-inheriting spouse for a Promissory Note for $500,000 & Deed of Trust securing that promise from the proceeds of the refinance or sale of the marital home. Failure to do so is presumed to be an irrevocable gift to the community. This is the difference between losing a quarter of a million dollars in a divorce versus getting the half million back before splitting the proceeds of the sale on top of that equally between spouses without a divorce court order.

The reason this applies even if the property is in only one spouse’s name is that the other spouse has a community property interest in the property regardless of title. To test this, just try to refinance or sell the property that is only in your own name after you get married. The first thing that will happen is you will need to get signed and record a Quitclaim Deed removing your spouse’s title interest in the property (but not their community property equity interest). If your spouse won’t sign, you can refinance or sell. It is as simple as that.

USE TO PAY OFF JOINT-TENANT FOR A QUITCLAIM DEED AFTER A DIVORCE OR BREAKUP

Whenever title to Real Estate is Transferred, either tax must be paid or an Exemption from Tax claimed.

Removing one Joint Tenant from a Property is done with a Quitclaim Deed which does not have Warranties like the Grant Bargain and Sale Deed that was used when you paid money for your property because you don’t need a promise that your spouse actually has an interest in your property. They do by virtue of marriage. They are giving up whatever they received by operation of law on the date of marriage regardless of the scope of the interest or how small it may be with the Quitclaim Deed.

The purpose of the Real Estate Excise Tax Affidavit (REETA) is to claim the Tax Exemption under the proper section of the Washington Administrative Code (WAC). You already paid several thousand dollars in tax when you bought your home, you don’t need to pay the tax again to remove a Joint Tenant from the Title.

YOU MUST GET SIGNED AND NOTARIZED, AND RECORD, A QUITCLAIM DEED AND REETA FROM YOUR SPOUSE IF YOU ARE AWARDED THE HOME IN A DIVORCE.

IF YOU HAVE NOT ALREADY BEEN PAID FOR YOUR EQUITY, YOU MUST RECORD A SIGNED AND NOTARIZED PROMISSORY NOTE AND DEED OF TRUST TO SECURE PAYMENT WHEN THE PROPERTY IS REFINANCED OR SOLD.

FAILURE TO EXCHANGE EQUITY FOR THE QUITCLAIM DEED LEAVES YOU VULNERABLE TO NEVER GETTING YOUR SHARE OF EQUITY IN THE HOME.

To Always Be a Human Being First, and My Role Second. To First, Do No Harm, then to provide the best legal outcome, smoothest process, best value, and to make a positive difference in the life of every client.

Christopher S. Mulvaney’s Mantra:

May I be filled with loving kindness for all life. May I be safe from dangers within and without. May I be healthy in body, mind, socially, and spiritually. May I be at ease and happy, doing good in the world.

May You be filled with loving kindness for all life. May You be safe from dangers within and without. May You be healthy in body, mind, socially, and spiritually. May You be at ease and happy, doing good in the world.

I am an experienced solo estate planning, debtor bankruptcy, and real estate attorney. At my law firm in Bellevue, Washington between Eastgate and Factoria, I do things a little differently. I am passionate about helping people take control of their lives.

One of my primary practice areas is urgent (bankruptcy), and the other is important, but not urgent (estate planning). Not letting the urgent crowd out the important is key. I have made a choice to include the positive difference I make in the life of each client in how I calculate profit. This means I have higher job satisfaction, and happy clients who confidently give referrals.

My goal is that my work is transformative for people during a challenging time in their lives. At Mulvaney Law Offices, PLLC (MLO), you will not find a gatekeeper. There are no forgotten cases hiding on an associate’s cluttered desk. It’s just me, working with each one of my clients one-on-one to resolve their legal concerns as favorably as possible.

As your lawyer, I will personally handle every aspect of your case. My office is not a factory churning out thousands of filings per year, where each case matters little. You, and your case, matter to me. You can see what clients have said about me, and leave your own reviews at these links.

Mulvaney Law Offices, PLLC is located in Bellevue, Washington, representing estate planning & chapter 7 and chapter 13 bankruptcy, clients in all 39 Washington Counties.

Washington State residents can meet with me in Zoom/DocuSign from anywhere in the world, and I can notarize their electronic signatures because I am a remote online notary. Just email me an image of your photo ID.