THIS WEBSITE INCLUDES GENERAL INFORMATION & THE OPINIONS OF CHRISTOPHER S. MULVANEY. IT IS INTENDED TO STIMULATE A BASIS FOR QUESTIONS RELATED TO YOUR PARTICULAR FACTUAL CIRCUMSTANCES — BEFORE YOU ACT. THIS WEBSITE DOES NOT CONSTITUTE LEGAL ADVICE. IF YOU WANT LEGAL ADVICE, PLEASE MAKE A ZOOM APPOINTMENT TO SPEAK WITH ME.

CONTACT CHRISTOPHER S. MULVANEY FORM

DISCLAIMER:

The use of email or this form for communication with MULVANEY LAW OFFICE, PLLC does not establish an Attorney-Client Relationship. If you don’t think I have responded, please check your spam folder. Time-sensitive information should not be sent through this Form or through email. Sensitive information can be uploaded to an encrypted Dropbox folder in your client file. Google Review LinkYelp Review Link

Gonzaga University School of Law – Spokane, Washington – Class of 2002 – Cum Laude The Latin phrase “Deo patriae, scientiis, artibus” translates to “For God and country through sciences and arts”. The initials A.M.D.G. on the seal of Gonzaga Law School stand for Ad Majorem Dei Gloriam, which is Latin for “For the Greater Glory of God” the Motto of the Society of Jesus (Jesuits): a Catholic religious order founded by St. Ignatius of Loyola.

_________________________

For real estate clients, lawyers should explain crucial tax issues, including capital gains and the Section 121 exclusion for primary residences, strategies for deferring taxes on investment properties such as 1031 exchanges, the tax implications of depreciation and depreciation recapture, and how passive activity loss rules can limit deductions.

Taxes on property sales

Capital gains and tax basis

Capital gains: When a client sells a property for more than its “tax basis” (its value for tax purposes), the profit is considered a capital gain and is generally taxable.

Holding period: How long a client holds the property determines the tax rate.

For a property held for more than one year, the gain is considered a long-term capital gain, which is typically taxed at a lower rate than ordinary income.

For a property held for one year or less, the gain is a short-term capital gain and is taxed at the client’s regular income tax rate.

Cost basis calculation: The tax basis of a property includes the original purchase price plus certain closing costs and the cost of capital improvements. Keeping careful records of all expenses is vital to accurately calculate the basis and reduce taxable gains.

Selling expenses: Costs associated with selling, such as real estate commissions, title fees, and attorney fees, can be deducted from the sale price to calculate the final gain.

Exclusion limits: Single clients can exclude up to $250,000 of gain, and married couples filing jointly can exclude up to $500,000.

Eligibility requirements: To qualify for this exclusion, the client must have owned and used the property as their main home for at least two of the five years leading up to the sale.

Exceptions and non-qualifying property: The exclusion has limitations if the property was ever used as a rental, was acquired through a 1031 exchange within the last five years, or if the client already used the exclusion within the last two years.

Real estate investment taxes

1031 like-kind exchanges

Tax deferral: Section 1031 of the Internal Revenue Code allows investors to defer capital gains taxes by reinvesting the proceeds from the sale of a business or investment property into another “like-kind” property.

Strict deadlines: This process requires adherence to strict deadlines:

The replacement property must be identified within 45 days of the sale.

The purchase of the replacement property must be completed within 180 days of the sale.

Qualified intermediary: A qualified intermediary is required to hold the sale proceeds; the client cannot touch the money directly, or the exchange will be disqualified.

Like-kind property: Like-kind is broadly defined for real estate, meaning a client can exchange a rental house for a commercial building, but the property cannot be their personal residence.

Depreciation and recapture

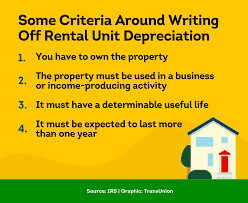

Deduction: The IRS allows real estate investors to deduct the cost of a property through depreciation, which accounts for the wear and tear of a building over time and lowers taxable income.

Residential properties are depreciated over 27.5 years,For U.S. tax purposes, residential rental property is depreciated over 27.5 years using the straight-line method under the General Depreciation System (GDS). This allows an investor to deduct a portion of the property’s cost each year, which reduces their taxable income.

How the 27.5-year depreciation works

Qualify the property. The property must be used for business or income-producing activity and have a useful life of more than one year. The average tenant stay must also be more than 30 days for it to be classified as residential property for this purpose.

Determine the depreciable basis. The calculation is based only on the value of the building and any capital improvements, not the land. The depreciable basis is the purchase price, plus certain closing costs, minus the value of the land.

Use the straight-line method. The depreciable basis is divided by 27.5 years to determine the annual deduction. For example, if the depreciable basis is $225,000, the annual deduction is about $8,181 ($225,000 / 27.5).

Calculate the deduction for the first year. The IRS uses a “mid-month convention” for the first and last years. This means depreciation is prorated based on the month the property was “placed in service”—or made ready and available for rent—with the property considered in service from the middle of that month.

Report the deduction annually. You continue claiming the deduction each year on your tax return until you have fully recovered your cost basis or you sell the property. The deduction is typically reported on IRS Schedule E.

How depreciation affects capital improvements

You must also depreciate capital improvements—such as a new roof, HVAC system, or addition—over their own recovery periods.

Minor repairs can be deducted in the year they are made.

Major improvements that add value, extend the property’s life, or adapt it for a new use must be depreciated.

Depreciation periods vary for different assets. For example, fences or driveways may be depreciated over 15 years, while appliances or furniture may be depreciated over 5 to 7 years.

Depreciation recapture and 1031 exchanges

Depreciation recapture: When you sell the property, the IRS “recaptures” the depreciation deductions you took and taxes that portion of the gain at a rate of up to 25%.

1031 exchange: You can defer the depreciation recapture tax by completing a 1031 exchange, which involves reinvesting the proceeds into another qualifying investment property.

while commercial properties are depreciated over 39 years.

Land is not a depreciable asset.

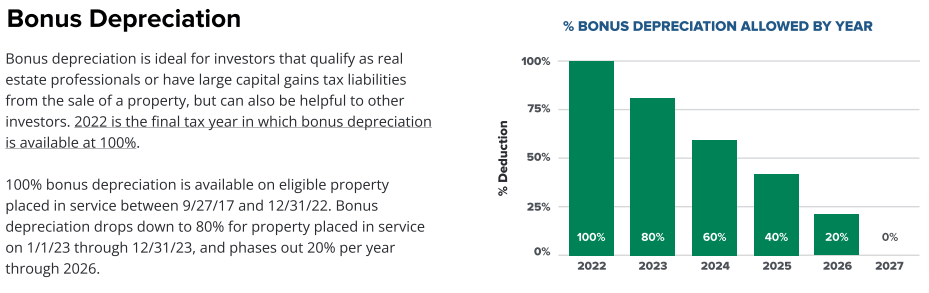

Bonus depreciation: The Tax Cuts and Jobs Act of 2017 created bonus depreciation, allowing immediate deductions for certain qualifying property.

However, this benefit is currently phasing out and scheduled to be fully phased out after 2026 unless extended by Congress.

Recapture: When a client sells a depreciated property, the IRS “recaptures” the depreciation deductions previously taken. Recaptured depreciation is typically taxed at a maximum rate of 25%, in addition to any capital gains tax on the remaining profit.

Passive activity loss (PAL) rules

Limitation on losses: Passive losses, which include most rental real estate losses, can generally only be deducted against passive income.

Exceptions for non-professionals: Clients who “actively participate” in managing their rental property may be able to deduct up to $25,000 in rental real estate losses against their ordinary income, but this allowance phases out completely if their modified adjusted gross income (MAGI) is over $150,000.

Real estate professional status (REPS): To deduct rental losses against ordinary income without limitation, a client can qualify as a “real estate professional” by meeting stringent time and participation requirements.

Other important tax considerations

Like-kind exchange for partnerships: For clients who own property through a partnership, the partnership entity, not the individual partners, must complete the exchange. Special rules apply if some partners want to participate in the exchange while others do not.

Opportunity zones: Clients can receive tax benefits by investing capital gains into a Qualified Opportunity Fund (QOF), which invests in low-income communities. These benefits can include deferring the initial capital gains and, if held for at least 10 years, excluding capital gains tax on any appreciation of the QOF investment.

Structuring property ownership: Lawyers can advise clients on the tax implications of different ownership structures, such as partnerships, limited liability companies (LLCs), or trusts. For instance, transferring property into or out of a partnership can trigger reassessment and affect taxes.

To Always Be a Human Being First, and My Role Second. To First, Do No Harm, then to provide the best legal outcome, smoothest process, best value, and to make a positive difference in the life of every client.

Christopher S. Mulvaney’s Mantra:

May I be filled with loving kindness for all life. May I be safe from dangers within and without. May I be healthy in body, mind, socially, and spiritually. May I be at ease and happy, doing good in the world.

May You be filled with loving kindness for all life. May You be safe from dangers within and without. May You be healthy in body, mind, socially, and spiritually. May You be at ease and happy, doing good in the world.

I am an experienced solo estate planning, debtor bankruptcy, and real estate attorney. At my law firm in Bellevue, Washington between Eastgate and Factoria, I do things a little differently. I am passionate about helping people take control of their lives.

One of my primary practice areas is urgent (bankruptcy), and the other is important, but not urgent (estate planning). Not letting the urgent crowd out the important is key. I have made a choice to include the positive difference I make in the life of each client in how I calculate profit. This means I have higher job satisfaction, and happy clients who confidently give referrals.

My goal is that my work is transformative for people during a challenging time in their lives. At Mulvaney Law Offices, PLLC (MLO), you will not find a gatekeeper. There are no forgotten cases hiding on an associate’s cluttered desk. It’s just me, working with each one of my clients one-on-one to resolve their legal concerns as favorably as possible.

As your lawyer, I will personally handle every aspect of your case. My office is not a factory churning out thousands of filings per year, where each case matters little. You, and your case, matter to me. You can see what clients have said about me, and leave your own reviews at these links.

Mulvaney Law Offices, PLLC is located in Bellevue, Washington, representing estate planning & chapter 7 and chapter 13 bankruptcy, clients in all 39 Washington Counties.

Washington State residents can meet with me in Zoom/DocuSign from anywhere in the world, and I can notarize their electronic signatures because I am a remote online notary. Just email me an image of your photo ID.